👋 Welcome back.

The new year has arrived quietly, along with renewed hope among crypto investors that the coming months might finally bring a meaningful shift in their favor. Some analysts estimate that Bitcoin could reach $120k–$200k by the end of Q2, with ETH in the $8k–$15k range, supported by regulation and institutional inflows, but with significant volatility risks, especially across smaller assets.

My own assessment, however, is more cautious. The current dynamics of the global economy do not yet appear to have reached the pace required for a clear and sustained bull market, of the kind many remember from 2020, when smaller altcoins delivered extreme upside. Several aspects of the current U.S. and global macro environment point in that direction.

This weekly note is about one thing only: figuring out whether the market currently favors altcoins or Bitcoin.

📬 In this issue:Global Liquidity Index (GLI): structure, trend, and implications

ISM PMI: what it says about the business cycle

Federal Reserve policy, rates, and forward guidance

Dollar strength (DXY) and its impact on crypto assets

Indicator synthesis and market regime assessment

Risk-On Environment Score (by Denomos)

Altcoins vs Bitcoin: regime-driven allocation

My portfolio positioning and key decision triggers

Before we dive in, one small favor:

If you find this post useful, consider hitting the ❤️ button or sharing the post. It helps this newsletter reach other crypto retail investors who are trying to make sense of the same question.

That’s it. Let’s get into the data.

Global Liquidity Index (by Denomos)

The concept of the Global Liquidity Index (GLI) was first introduced by Michael J. Howell, founder and CEO of CrossBorder Capital. CrossBorder Capital publishes regular weekly GLI estimates, covering liquidity data from roughly 80 of the world’s largest economies, including central banks, the private sector, shadow banking, and cross-border capital flows.

GLI gained significant popularity among crypto investors largely due to Raoul Pal, as it has shown a strong historical correlation with both equity and crypto market expansions and contractions.

On the Denomos platform (full disclosure: I am a co-founder), a less complex (but still highly accurate!) version of GLI is available and used throughout my analysis. The current GLI reading on Denomos stands at approximately $150.4T, representing a slight decline compared to December. While the trend has remained positive since December 2024 without major corrections, the pace of liquidity expansion is not strong enough to trigger an altcoin season comparable to 2020.

At that time, liquidity growth exceeded 15% YoY, reaching those levels within just a few consecutive months. As of November, year-over-year liquidity growth across the world’s twenty largest economies stood at approximately 7%, marking a mild slowdown compared to June, when YoY growth was around 8%.

showing the level and trend of worldwide liquidity from 2022 to 2026, as calculated by Denomos.")

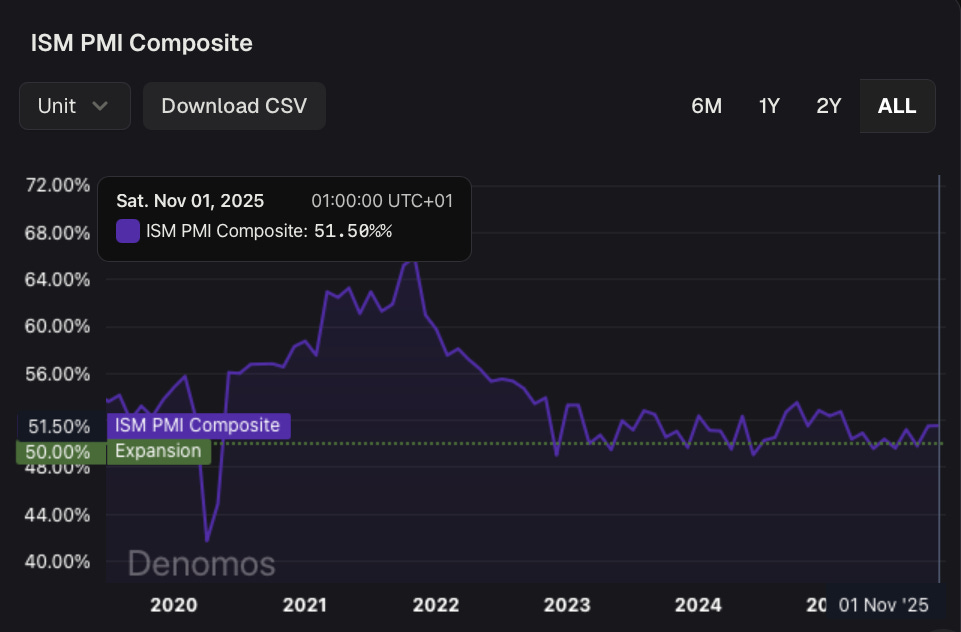

ISM PMI

The PMI (Purchasing Managers’ Index) is an economic indicator based on monthly surveys of purchasing managers in private companies. It is used to assess business conditions in the manufacturing and services sectors. PMI is widely applied to anticipate economic trends such as GDP growth, employment, and inflation, since purchasing managers have early insight into changes in supply chains, orders, and pricing. As such, PMI is considered one of the most important leading economic indicators for global markets, offering an early signal of overall economic health.

Most major economies publish their own PMI data, including the United States, China, EU member states (such as Germany, France, and Sweden), Japan, the UAE, Russia, and others. The main data providers include S&P Global (for most countries), ISM (for the United States), Caixin (for China), and various local institutions.

ISM PMI is the U.S.-specific version of PMI published by the Institute for Supply Management (ISM). It is a monthly index based on surveys of more than 400 purchasing managers across 20 industries in the manufacturing sector. ISM also publishes a separate Services PMI covering the U.S. services economy.

In simple terms:

Readings below 50 indicate economic contraction

Readings above 50 typically signal economic expansion

Beyond absolute levels, the trend of the index provides critical additional context.

PMI is also highly relevant for crypto markets. Although altcoins are not traditional companies, their performance has historically been closely correlated with business cycle dynamics and equity markets.

On the Denomos platform, both Manufacturing and Services ISM PMI are tracked and combined into a composite index. At present, the ISM PMI Composite stands at 51.5 and has been moving sideways within a range of approximately 49–53.5 for nearly three years (since December 2022). This prolonged sideways behavior, combined with readings only marginally above 50, is not sufficient to initiate an altcoin season.

For context, the 2020 altcoin cycle began roughly four months after the ISM PMI Composite surged sharply from 41.7 to 56.7, following aggressive quantitative easing and interest rate cuts to zero by the Federal Reserve.

Fed

The United States remains the most dominant economy in the world, and that economy is directly shaped by the Federal Reserve and its monetary policy. Given that the largest share of crypto capital is held by U.S. investors and institutions and that the new U.S. administration is actively positioning the country to remain (or become) a global crypto hub, every Fed decision tends to trigger a visible reaction in crypto markets.

One relatively recent and positive development is that the Federal Reserve ended its Quantitative Tightening (QT) phase (which had been in place since 2022) toward the end of November 2025. Since December, the Fed has shifted into a phase of “balance sheet maintenance and mild expansion” through so-called Reserve Management Purchases (RMPs). While the Fed maintains that this does not constitute full Quantitative Easing (QE) (but rather precautionary measures to ensure sufficient reserves in the banking system and avoid liquidity stress events like those seen in 2019), any balance sheet expansion can be interpreted as a form of QE, which is generally supportive for risk assets, including altcoins. However, while the resumption of balance sheet expansion may gradually shift market conditions in favor of risk assets, a stronger impulse would likely be needed to fully change the regime.

Moreover, the current Federal Funds Rate stands at approximately 3.6%, while the real interest rate is around 0.8%. Historically, both levels are associated with non–altcoin-season conditions. Past cycles suggest that strong altcoin rallies typically require real interest rates to move below 0%, ideally while also trending downward.

According to the Summary of Economic Projections (SEP) released on December 10, 2025 (following the December FOMC meeting), the Federal Reserve expects inflation to remain under control over the next 6–12 months, with unemployment potentially drifting slightly lower. That said, risks related to geopolitics or trade tariffs could still introduce new shocks to the economy. The next scheduled Federal Open Market Committee (FOMC) meeting will take place on January 27–28, 2026, when policymakers will assess the possibility of further interest rate cuts. Such a move could act as an additional catalyst toward a more pronounced risk-on environment, depending on the broader macro backdrop.

DXY

Since January 2025, the DXY has been in a downtrend. In April, it broke below a key support level near 100 and has since been trading within a range between 96 and 102.

This development is generally positive for risk assets, as a weakening dollar often coincides with capital flows into riskier asset classes.

Whether this trend continues remains to be seen. However, it is worth noting that the U.S. government has a strong incentive to maintain a weaker dollar in order to manage its rapidly growing debt burden, which currently stands at approximately $36.21 trillion. 🤯

daily chart showing a prolonged range below the 100 level, with weakening momentum and uncertainty about a potential continuation lower, highlighting implications for global risk assets.")

Indicator Synthesis

When combining all of the indicators discussed above, the conclusion is clear: the market has not yet entered a full risk-on regime. Current conditions continue to favor asset classes with lower relative risk.

A broad and sustained rally in smaller crypto projects would require a meaningful shift in these macro dynamics. It also remains uncertain whether a liquidity environment comparable to 2020 is even achievable again without a significant crisis forcing the Federal Reserve into aggressive QE.

Risk-On Environment Score (by Denomos)

On the Denomos platform, users have access to the Risk-On Environment Score, which combines all of the indicators discussed above into a single, coherent index. The purpose of this score is to make market conditions easier to interpret for retail investors. Historically, it has proven to be a reliable signal, as sustained moves above 80 have closely aligned with the beginning of genuine bull markets in digital assets.

The current score stands at 62.39, showing a mild upward trend since January 2025.

This provides additional confirmation that current market conditions are not yet supportive of broad exposure to high-risk crypto assets.

Score chart from 2017 to 2026, showing cyclical shifts between risk-on and risk-off environments, with the current reading near 62 indicating a transitional market regime.")

Altcoins or Bitcoin? A Regime-Based Conclusion

This is not financial advice. Do your own research. Investing in digital assets is risky.

Based on everything discussed above, my current allocation decision is regime-driven and non-ideological. Under present market conditions, that decision clearly favors Bitcoin.

Bitcoin offers lower relative volatility, deeper liquidity, and has managed to sustain a meaningful bull run even under tightened financial conditions over the past three years. It recently revisited its all-time highs, and the question is not if, but when that level may be reached again. Current estimates range between $120k and $200k in the first half of the year, representing approximately 40–150% upside from current levels (which is more than sufficient upside potential for me, given today’s macro environment 😅).

Altcoins, for now, will need to wait before a meaningful portion of my capital is allocated to them.

Portfolio Positioning & Performance

At present, my portfolio is allocated 100% to Bitcoin.

I began publicly sharing my portfolio just over a week ago (in this post), when Bitcoin was trading at $88,336. At the time of writing, BTC is priced at $90,585, which puts the portfolio at a modest +2.52% since inception.

I will continue to share my portfolio performance publicly on Substack going forward. In the coming weeks, I also plan to outline the altcoins I am monitoring, waiting for market conditions to shift in their favor before allocating capital.

Closing Words

All of the indicators discussed in this newsletter are part of the analytical framework we are building at Denomos.

This includes a simplified but robust Global Liquidity Index, constructed from central bank balance sheets, M2 money supply, the Treasury General Account, RRP, and liquidity dynamics across the world’s 20 leading economies, updated weekly, with both cumulative levels and YoY changes to better capture liquidity momentum. It’s less complex than institutional products like CrossBorder Capital, but significantly more accessible, and far more informative than generic TradingView indicators.

We also track ISM PMI data (services and manufacturing), combined into a composite index with a weighted structure that better reflects the U.S. economy, alongside YoY dynamics to capture changes in business conditions over time. In addition, all key Federal Reserve data (rates, balance sheet, forward guidance, etc.) are available in one place, with notifications when new data is released.

These inputs are synthesized into a single Risk-On Environment Score, designed to signal when market conditions structurally shift toward or away from risk-taking, along with alerts when key thresholds are crossed.

Thanks for reading. If you have thoughts, questions, or disagree with any part of the analysis, feel free to share them. ✍️

And if you’d like to be notified when the next Altcoins vs Bitcoin analysis is published, consider subscribing. 🍻

I wish you a healthy New Year! 🫂